Your Ultimate Limited Company Expense Claim Guide for 2026

- redparrotuk789

- Jun 15

- 7 min read

Claiming legitimate business expenses is one of the most effective, legally sound methods for a limited company director to optimize profits and structurally reduce a Corporation Tax liability. However, successfully extracting value through expenses relies entirely on a deep, precise understanding of current UK tax legislation.

For the 2026/27 tax year, HM Revenue & Customs (HMRC) has implemented several structural policy updates—including a monumental change to business mileage allowances that ends a 15-year freeze. Failing to adapt your bookkeeping to these new thresholds can result in missing out on thousands of pounds in valid tax relief, or worse, triggering an invasive HMRC compliance audit.

This comprehensive, expanded guide from Red Parrot Accounting Ltd breaks down the essential expense categories every limited company director in Swindon, London, and the wider UK needs to master to safely protect corporate profits while maintaining total statutory compliance.

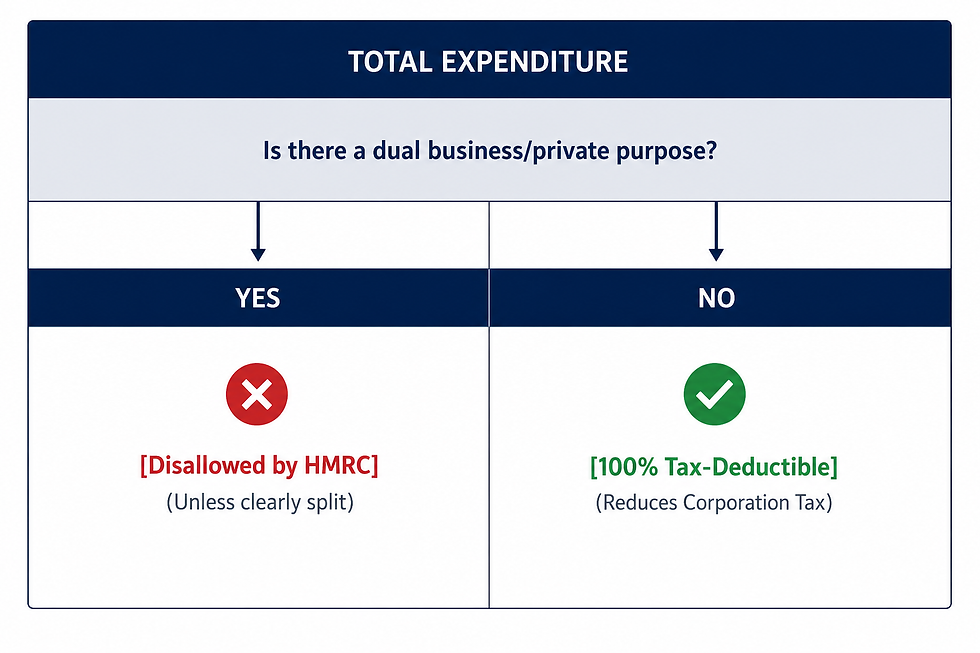

The Core Rule: "Wholly and Exclusively"

Before reviewing specific expense categories, every director must understand the underlying legislative principle that governs all business deductions. Under UK tax law, for an expense to be considered tax-deductible against your company’s trading revenue, it must be incurred wholly and exclusively for the purposes of your trade.

Breaking Down the Legislation

The "wholly and exclusively" mandate focuses strictly on the core motivation behind the transaction at the exact moment the funds were spent.

Wholly focuses on the quantum or the portion of the expense. If a specific purchase is split between business operations and personal life, you cannot simply claim the full invoice value. However, if you can clearly and fairly isolate the business usage (such as itemized costs on a mixed-use mobile phone contract), that specific portion can be cleanly claimed.

Exclusively targets the primary intent. If an expense carries an inherent dual purpose that cannot be separated, the entire deduction will fail HMRC scrutiny.

The Everyday Clothing Example

A classic point of confusion for new directors is everyday business clothing. Even if you buy a high-end suit specifically to wear to a client pitch in Central London, the suit serves an unavoidable personal purpose: keeping you warm and maintaining basic decency. Because this dual-purpose nature cannot be separated, the suit is completely disallowed for Corporation Tax purposes.

Conversely, specialized protective gear, safety boots, or branded corporate uniforms displaying a prominent company logo are 100% claimable because their fundamental utility is business-specific.

Travel and Subsistence Rules (The Huge 2026 Update)

Corporate travel remains one of the most heavily scrutinized areas during HMRC tax inspections. Fortunately, the government introduced a major policy shift backdated to 6th April 2026 designed to help business owners combat rising vehicle maintenance and fuel costs.

The New 2026 Approved Mileage Allowance Payments (AMAP)

For the first time since 2011, the Approved Mileage Allowance Payment rate for cars and vans has officially increased. Directors utilizing their personal vehicles for business journeys can now claim significantly higher tax-free reimbursements directly from the company:

Vehicle Type | First 10,000 Business Miles | Over 10,000 Business Miles |

Cars & Vans | 55p per mile (Up from 45p) | 25p per mile (Unchanged) |

Motorcycles | 24p per mile (Unchanged) | 24p per mile (Unchanged) |

Bicycles | 20p per mile (Unchanged) | 20p per mile (Unchanged) |

💡 The Passenger Bonus: If you are driving a personal car or van for an approved business trip and carry a fellow employee or co-director along for the journey, you can claim an additional 5p per mile per passenger tax-free. This is an exceptional, often overlooked incentive for team travel to regional client sites.

Commuting vs. Genuine Business Travel

To claim mileage or public transit costs safely, you must understand how HMRC differentiates a regular commute from a business journey.

Ordinary Commuting: Travelling between your residential home and your designated permanent workplace or main corporate office is classified as ordinary commuting. If your registered limited company office is located in Swindon and you drive there every morning, those miles are personal expenses and cannot be run through the business ledger.

Temporary Work Locations: Travel undertaken to a location that is temporary (where you spend less than 24 consecutive months) is fully deductible. If a Swindon-based consultant travels up to London to attend a specific project meeting or pitch to a new client, the entirety of that round-trip transit—whether via the M4 or Great Western Railway—is 100% claimable.

Subsistence and Overnight Stays

When traveling for genuine business purposes, your company can legitimately cover the cost of reasonable meals, refreshments, and hotel accommodations. However, "subsistence" is not a blank check for extravagant dining. HMRC expects these expenses to mirror the ordinary standard of living required to execute the trip. Always ensure itemized receipts are preserved alongside a quick calendar note outlining the business rationale for the trip.

The Home Office Reality in 2026

With hybrid and distributed corporate frameworks completely dominating the 2026 business landscape, managing home working deductions correctly is essential for optimizing your personal tax profile. As a director running an active limited company from home, you can extract overhead relief using two primary, mutually exclusive methods:

Method A: The Simplified Flat-Rate Allowance

HMRC provides an administrative shortcut by allowing a flat-rate deduction of £6 per week to cover incremental household utilities.

The Advantage: It is incredibly straightforward, completely automated within your accounting software, and requires absolutely zero tracking of utility invoices or space calculations.

The Disadvantage: At roughly £240 to £312 per year, it rarely reflects the true operational cost of heating, lighting, and powering a tech-heavy home office across a full year.

Method B: The Formal Rental Licence Agreement

If you utilize a distinct, dedicated portion of your home exclusively to run your limited company operations, your business can enter into a formal commercial relationship with you as an individual landlord.

Under a Rental Licence Agreement, your company pays you a structured monthly rent to occupy that workspace. This rental rate must be meticulously calculated based on a fair proportional split of your actual home expenditures (such as square footage calculations of your rent, mortgage interest, council tax, and internet connectivity) and must strictly match fair market values for equivalent local commercial workspaces.

⚠️ The Personal Tax Catch: While this rental payment is a 100% valid deduction that successfully drops your company’s taxable net profits, that rental income does not vanish. You are legally required to declare this rent as property income on your personal Self Assessment tax return each year. If not structured precisely with a professional accountant, you risk accidentally drifting into higher personal income tax bands or complicating your primary residence Capital Gains Tax exemptions when selling the property.

Tech, Tools, and Corporate Capital Equipment

In our highly digitized economic landscape, maintaining an infrastructure of modern software, reliable hardware, and mobile connectivity is a core operational necessity.

Laptops, Hardware, and Capital Allowances

Any computing hardware, specialized machinery, or executive office furniture purchased directly by your business is recognized as a fully claimable corporate asset. For technology assets, you will leverage Capital Allowances within your year-end reporting to immediately offset these capital investments directly against your taxable trading profits, matching the true economic lifespan of the device.

The "Name on the Contract" Trap

The most critical compliance mistake directors make in this area centers on software subscriptions (like cloud accounting systems, CRM tools, and creative design suites) and mobile phone lines.

To be cleanly written off against Corporation Tax, the underlying contract and billing account must be explicitly registered in the limited company’s legal name, and paid out of your corporate bank account. If you sign up for a premium software package or a smartphone line using your personal name and credit card, HMRC views the company’s reimbursement of that cost as a personal benefit in kind (BiK). This mistake triggers complex payroll processing requirements, employee National Insurance exposure, and unnecessary administrative adjustments.

Staff Welfare vs. Client Entertaining

Maintaining exceptional team morale and managing external commercial relationships require two fundamentally different accounting approaches under UK tax law.

The Tax-Free Staff Entertainment Allowance

HMRC awards limited companies an annual tax exemption designed specifically for hosting social events for employees and directors, such as a traditional summer gathering or an end-of-year holiday celebration:

The Allowance: You can claim up to £150 per head, per year (inclusive of gross VAT).

The Spousal Inclusion: This allowance fully extends to regular life partners and spouses, meaning a director and their partner can comfortably enjoy up to £300 of company-funded entertainment across the financial year, provided the event meets the basic social criteria.

🚨 The Hard Cap Warning: The £150 figure is a strict regulatory threshold, not an allowance. If a corporate event finishes with an official total cost averaging out to exactly £151 per attendee, the entire event loses its exempt status. The whole £151 immediately becomes treated as a taxable benefit in kind, exposing your staff members to personal income tax penalties and forcing the company to pay unexpected National Insurance charges.

The Client Entertaining Reality

While rewarding your hard-working staff is heavily incentivized under the tax code, taking clients, key prospects, or industry suppliers out for dinners, drinks, or sporting events follows a completely different script.

While it is entirely legal and normal for your limited company to pay for client entertainment directly from its bank account to build business relationships, these costs are completely non-deductible for Corporation Tax purposes. They must be flagged and added straight back into your taxable profit calculations during your year-end filing cycle.

Record-Keeping and Digital Receipts

An expense claim is only as solid as the digital paper trail supporting it. Under current UK statutory frameworks, limited company directors carry an absolute legal obligation to preserve all records of business transactions, purchase invoices, and receipts for a minimum of six years from the end of the relevant accounting period.

Navigating Modern Audits

In 2026, relying on faded paper slips stuffed inside a drawer is an operational liability. If HMRC chooses to launch an official inquiry into your corporation’s filings, you must produce clear, unedited, legible records validating the exact date, vendor details, tax breakdown, and core commercial rationale behind every single transaction.

The most secure, efficient strategy is adopting an automated, cloud-based receipt capture application integrated directly with your bookkeeping engine. Taking a quick smartphone photo of a vendor invoice at the point of sale preserves the data digitally in real-time, attaches it directly to the corresponding bank transaction, and completely protects your company from missing out on valid deductions.

Bulletproof Your Company Expenses Today

Optimizing your business expenses requires balancing growth with strict compliance. Identifying every valid deduction allows you to retain more capital to reinvest directly back into your company's expansion, while staying clear of unexpected penalty traps.

At Red Parrot Accounting Ltd, we help limited company directors maximize their tax efficiencies seamlessly. Based across Swindon, London, and the wider UK, our corporate tax specialists work alongside you to review expense frameworks, implement automated receipt management systems, and build structured, long-term tax planning strategies that protect your bottom line.

Ready to maximize your business deductions safely under the latest 2026 tax rules? Contact the corporate tax planning experts at Red Parrot Accounting Ltd today to schedule a comprehensive expense audit.

Comments